2022 Projected tax revenue versus projected actual

In the 2022 Budget, the main budget revenue for 2022/23 was projected to be R1.6 trillion. South

African Revenue Service (SARS) is now expected to collect tax revenue amounting to R1,69 trillion for 2022/23, an amount which is R93.7 billion higher than the budgeted revenue. The positive variance of R93.7 was a result of better-than-expected collections mainly from the mining sector due to the sector experiencing favourable high commodity prices. A continued recovery from the pandemic among companies in the manufacturing and financial sectors also contributed to this strong revenue performance. An increased tax revenue without corresponding tax increases serves as an indication that the enforcement tools (tax audits and imposition of penalties) deployed by SARS are starting to bear fruits.

2023 projected revenue

The main tax revenue for the 2023/24 fiscal year is projected to be R1.8 trillion or

25.1 per cent as a share of Gross Domestic Product (GDP) in 2023/24. The attainment of this tax

revenue target is based on the projection that South Africa will achieve a real economic growth of 0.9% for 2023. The ability of the Treasury to correctly project the performance of the economy has direct bearing on whether the tax revenue will be collected or not.

The tax-to-GDP is projected to reach 25.4 percent in 2022/23 and expected to reach 25.7 by 2025/26. These percentages are still low as compared to Organisation for Economic Cooperation and Development (OECD) countries average tax-to-GDP of 34.1%.

MAIN TAX PROPOSALS FOR BUSINESSES AND INDIVIDUALS

Businesses are currently experiencing financial hardships caused by poor economic growth and

unreliable electricity supply. Much to the taxpayers’ relief, the Minister has announced that no

significant tax increases will be proposed.

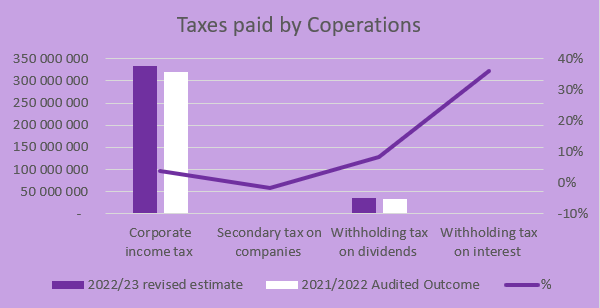

Corporate Income Tax (CIT)

The CIT rate is currently at 27%. No proposed changes to this rate.

Research and development incentives

The research and development incentive was due to end on 31 December 2023. There is now proposal to extend this incentive for 10 years from 1 January 2024.

Expansion of the renewable energy tax incentives

Currently, businesses are allowed to claim costs of the qualifying investment in wind power and

concentrated solar energy over a period of three years (50% in year 1, 30% in year 2, and 20% in year 3) in terms of section 12B of the Income Tax Act. The Budget proposed a change to the incentive that will allow businesses to claim 125% of the costs of the qualifying investments in renewable energy with no thresholds on generation capacity in the first year.

Capital Gain Tax (CGT)

CGT is triggered by a disposal or deemed disposal of an asset. The effective rate of CGT remains at 22.4% for companies. No proposed changes.

Value Added Tax

VAT is levied at the standard rate of 15% on the supply of goods and services by registered vendors. No changes in the VAT rate were proposed.

Dividends Tax

Dividends tax is a final tax on dividends at a rate of 20%. No changes were proposed.

Carbon Tax

The carbon tax rate increased from R144 to R159 per tonne of carbon dioxide equivalent, effective from 1 January 2023. The carbon fuel levy for 2023 will increase by 1c to 10c/l for petrol and 11c/l for diesel from 5 April 2023, as required by legislation. It is proposed that the carbon tax cost recovery quantum for the liquid fuels refinery sector increases from 0.63c/l to 0.66c/l from 1 January 2023.

Rooftop Solar tax incentive

To increase electricity generation, the Minister proposed a rooftop incentive for individuals to invest in Solar PV panels. Individuals will be able to claim a tax rebate against their tax liability to the value of 25% of the cost of any new and unused solar PV panels, subject to a maximum amount of R15 000. This incentive will be available for one year, that is, from 01 March 2023 to 29 February 2024.

Revenue Projections

Overall

The Minister has announced that the revised tax revenue target for the 2022/23 is now R1.69 trillion form 1.59. The increase is attributed to broad-based corporate tax recovery in the second half of 2022/23 particularly in the financial and manufacturing sector despite softening commodity prices.

In addition, an improved tax compliance levels and efficiency in the tax administration is also noted to have contributed to the improved tax revenues. To this end, the National Treasury kept its promise to not raise taxes or introduce a new wealth tax fill any tax gap.

The main tax revenue for the 2023/24 fiscal year is projected to be R1.787 trillion or 25.7 per cent of the Gross Domestic Product (GDP). To achieve the estimated tax revenue for 2023/24, the National Treasury expected that the real economic growth will average 1.4 for 2023.

Indirect Taxes

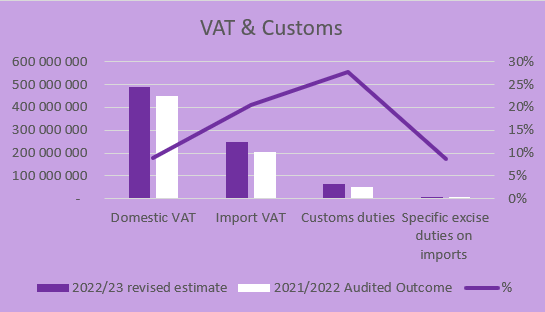

VAT, Customs & Excise

![]()

Increase in Import VAT possibly due to increase in online activity. Where online sales are the main driver to the Policy makers may over team need to consider impact on local industries…not comment was provided by the Finance Minister on the main drivers of Import VAT.

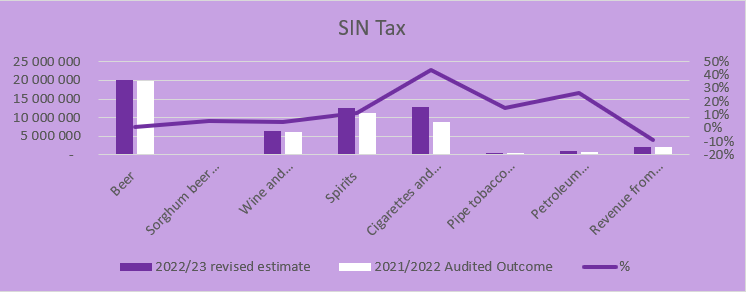

![]()

Increase related to Cigarette and tobacco related to increase in SARS enforcement activity

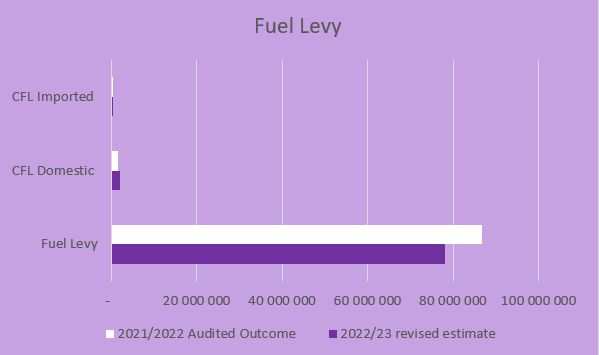

![]()

Decrease in fuel levy due temporary reduction of rate from 6 April to 6 July 2022 of

R1.50 per letter and reduction of R0.75 from 7 July 2022 to 2 August.

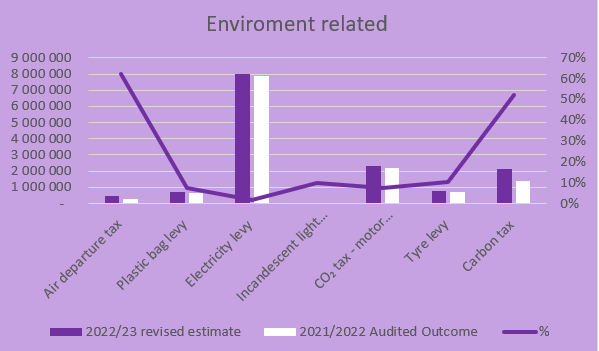

![]()

![]()

![]()

Tax Statistic

Heading Tax to GDP ratio

The tax-to-GDP ratio is a measurement of the country’s share of tax collection relative to the GDP. The higher the percentage, the higher the amount of tax revenue collections relative to the country’s economy. A tax-to-GDP ratio of 25.4% is expected in the 2022/23, higher than the 24.7 per cent in the 2022 Budget Review. The ratio was 26,3 per cent of GDP before the pandemic, which indicate that the country has not fully recovered from the pandemic, especially small and medium enterprise that continue to operate on a shoestring budgets and margins.

In what appeared as an unexpected move, the International Monetary Fund (IMF) has recently reported a slightly increase in the growth projections for the South African economy. According to IMF the economic growth is expected to reach 1.2% in 2023, an increase of 0.1%

A high tax-to-GDP ratio is an expression of a higher economic growth, durable economic activities and improvement in the tax compliance levels. A high tax-to-GDP ratio can be achieved, especially where taxpayers believe that they receive good value for their money, however, this is currently not a case in South Africa.

South Africa has a relatively high tax-to-GDP ratio compared to other developing countries. Although the country is expecting to achieve GDP growth of 2.5 percent in the 2023 to 2025, unless government takes urgent measures to reduce loadshedding and improve energy capacity, the economic growth prospects remain under an enormous threat.

Debt level

The gross debt stock is projected to increase from 4.73 trillion in 2022/23 to R5.84 trillion in 2025/26. Due to the increase in the gross debt, the debt-service costs were projected to be higher reaching an average R366.8 billion annually over the medium term and expected to reach R397.1 billion in 2025/26. The resources obtained are said to be otherwise used to address the pressing social needs, or to invest in the country’s future. This aligns to the government’s spending in which indicates that of more than half of the governments consolidated expenditure will be spent on social services.

Despite the increase in the government expenditure accompanied by the increase in gross debt, there seems to have been a decrease in the fiscal deficit which is said to be due to the revenue that is higher than expected. This seems to be good news for the country as the reduction in the fiscal deficit was reduced without tax increases or cuts in the social wage and infrastructure. This is also a clear indication that the government is heading in the right direction in addressing the sovereign default risk.

Economic Outlook

Download it here

To view the full article, click here [ 588 kb ]