Did you know South Africa has a VAT concept called “Flash title sale? This concept involves a South African registered vendor selling its movable goods to a foreign customer

who is not registered for VAT in South Africa.

These movable goods are not intended to be delivered by the RSA Vendor to the foreign country i.e. they remain in South Africa (within the designated ports) post the sale. That foreign customer in return sells the same movable goods to another foreign customer(s).

In between the sale, the movable goods are stored in the bounded warehouse in the customs-controlled area in South Africa until the second foreign customer makes a collection.

Who are the 'Qualifying Purchasers'?

In between the sale, the movable goods are stored in the bounded warehouse in the customs-controlled area in South Africa until the second foreign customer makes a collection. The Foreign purchasers are defined as a “Qualifying Purchasers” in the export regulation (GNR.316 of 2 May 2014). Goods sold to a Qualifying Purchaser may be subject to VAT at a zero rate where all other requirements are met.

A “Qualifying Purchaser” can write to the Commissioner requesting not to be classified or recognised as a “Qualifying Purchaser”. Where this is the case, the supply of goods will be treated as a normal standard sale within the borders of South Africa i.e. the RSA vendor will be required to impose VAT at the standard rate (15%).

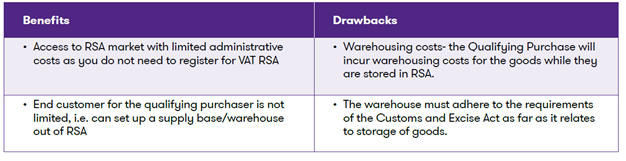

The benefits and drawbacks for Qualifying Purchasers:

![]()