Interest rate stress impacting consumption - H1 2023

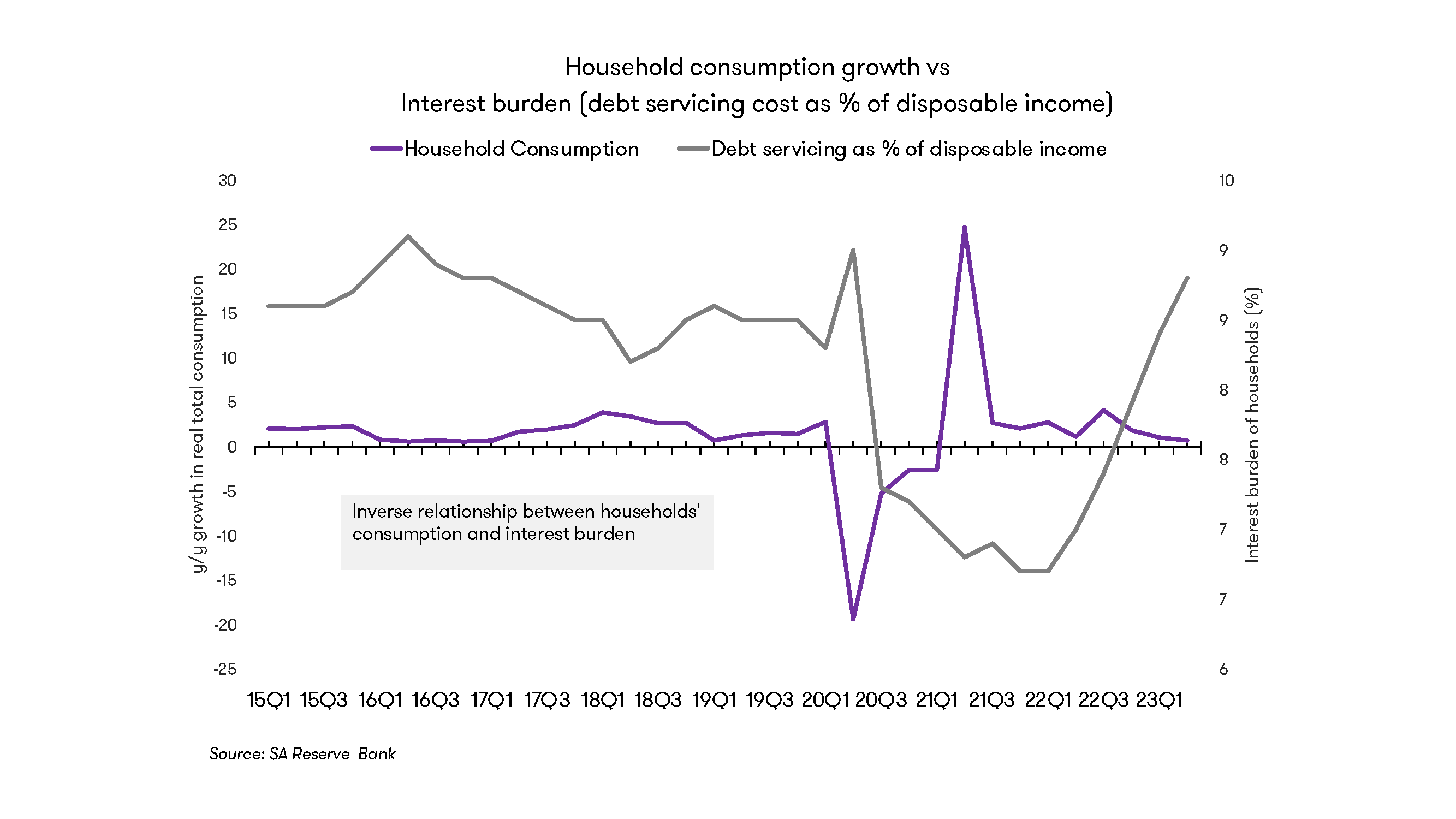

The fact that interest rates have risen around 5% over the past two years has begun having a meaningful adverse impact on consumer spending. Growth in household consumption expenditure contracted by -0.7% y/y in Q2 after growing by 2% and 5% in 2021 and 2022.

Retail sales fell by almost 2% in 2023 due to worsening consumer finances. Impairments from unpaid consumer accounts increased. Household credit demand, which had a steady growth in 2022, declined progressively throughout 2023 to its lowest point in two years.

The high level of interest rates has finally started acting as a deterrent to taking on debt amongst financially stressed consumers. Fortunately, the household debt to disposable income ratio has edged up only marginally, mainly due to recent negative growth in disposable income. The ratio is nonetheless no way near the highs witnessed a decade ago.

Whereas much of the initial decline in growth of consumer spending was evenly spread across all segments of consumption, recent data suggest that the demand for discretionary goods is now falling off considerably faster than other areas of consumer spending. Growth in passenger vehicle sales, for example, is now substantially negative, having been positive earlier in the year.